For markets this week, we are looking at the past week’s economic data releases and providing some color on recent moves within the oil markets.

September: Labor Market Strengthens, Inflation Moderates

Last month’s jobs report came back much stronger than anticipated. The survey estimated 150,000 new jobs, a 4.2% unemployment rate and average hourly earnings YOY of 3.8%. The actual report reflected 254,000 new jobs, a 4.1% unemployment rate and average hourly earnings YOY of 4.0%. It also featured an upward revision of August’s nonfarm payrolls number by 17,000 jobs.This created volatility in the interest rate market, with rates rising across the board. The market moved from pricing in three interest rate cuts in 2024 to two, signaling a 25bps cut at each of this year’s remaining meetings. One report shouldn’t change the narrative, but it does underscore that the labor market is still tight. Between last week’s port strike and the recent catastrophic hurricanes, a weaker October report is on the table.

Thursday morning, we received the latest CPI report. The September report showed a narrow miss of expectations, with CPI coming in at a year-over-year increase of 2.4% versus the survey response of 2.3%. This is a slight miss on expectations, and the market seems to be taking it in stride given it is still a decrease from August.

Things could get complicated for the Fed if there is meaningful strengthening in the labor market in tandem with an increase in inflation. As always, we want to fit these reports into the broader context of the market and try to separate the trend from the noise. The trend of a strong labor market paired with decreasing inflation remains intact for now.

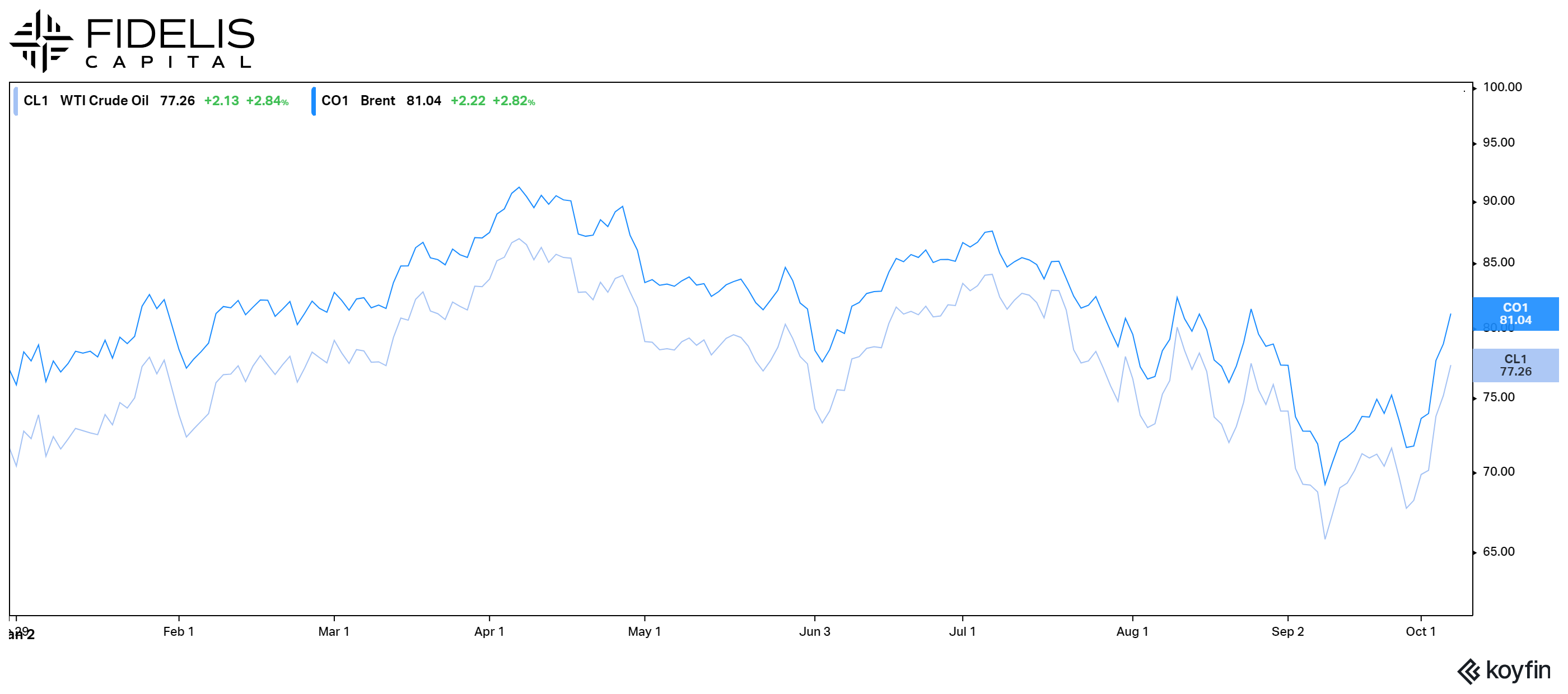

Oil Prices Finally Respond to Geopolitical Events

Going back through history, oil prices tend to react to geopolitical risk by increasing. For example, we saw Brent crude oil futures rise from a low of $69.80 at market open on December 2, 2021, to a high of $130.28 at market open on March 8, 2022, in response to Russia’s invasion of Ukraine.Western markets worked to exclude Russian energy from their imports, causing the overall supply to fall and prices to rise. As time progressed, other members of the global energy community increased their supply, which ultimately led energy prices back into the ~$70-$90 range at the beginning of 2023.

The resilience of oil prices throughout the recent conflict in the Middle East has been noticeable. Earlier this year, we saw Brent crude oil prices trade up to $90 in April during the initial Iranian attack on Israel then fall back down over the summer. The price chart below shows how Brent crude oil futures and West Texas Intermediate crude oil futures have behaved so far this year.

Keep in mind that Brent measures oil prices from the North Sea and is used as a proxy for international energy prices, while West Texas Intermediate measures oil prices from the U.S.

This week, following the most recent Iranian attack, we saw oil start to spike again. Initial resilience was spoiled as rumors began to float that Israel was considering attacking Iranian oil facilities (in lieu of Iranian nuclear facilities), which would cause supply disruptions.

With the ongoing conflict, another major factor that has led to lower oil prices has been disagreements within OPEC+ on production. OPEC+ is a group of oil-producing countries that coordinate their energy policy, typically with an effort to bolster oil prices. It was recently reported in the Wall Street Journal that Saudi Arabia warned other OPEC+ members about producing more oil than their commitments, which, if continued, could lead to an oversupply negatively impacting prices. Specifically, Iraq, Kazakhstan and Russia are under the microscope.

Back in 2020, Russia and Saudi Arabia were embroiled in a price war, which caused Saudi Arabia to flood the market with oil. During this timeframe, there was a period where the oversupply was so drastic that oil futures went negative, indicating that distributors were willing to pay investors to take their oil. The current disagreement does not appear to be as drastic, but we are watching closely as these two supply-side issues unfold.