By: Aaron Wall, CFA

Partner, Portfolio Manager

Interesting headlines across key themes we’ve been covering in Insights—AI, changes at the Fed, the state of the economy—stood out this week.

Strada: AI and Entry-Level Jobs

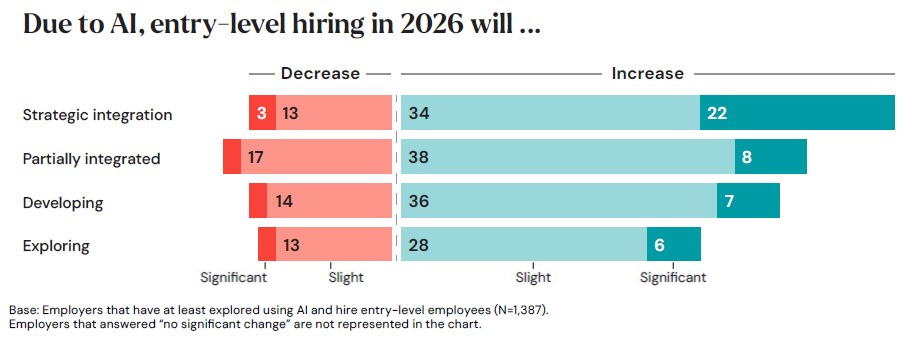

Strada, a foundation focused on education, released a report earlier this week called, “Entry-Level Hiring in the AI Era: What Employers Are Thinking (and Doing)”. The company surveyed nearly 1,500 senior executives about how their hiring practices are adapting to the new AI environment.As AI continues its long road to integration within businesses, fears are mounting that it may quickly displace entry-level job openings, which are traditionally for college graduates. Since we are still in the very early stages of this new technology, watching how it disrupts this group serves as an important benchmark for how AI can impact the labor market.

The survey results are broken down by the firm’s current usage of AI in the broader business, as seen in the chart below.

Source: Strada

The counterargument to fears about job displacement is that, throughout history, capitalism has always gone through cycles of creative destruction. When productivity increases, goods tend to get cheaper and demand tends to increase over time. There is no doubt that AI will drive disruption, but how we respond will be critical.

In Strada’s survey, 57% of technology companies and 39% of all other companies cited that AI tools were actually increasing the demand for entry-level jobs.

This makes sense. They want to use AI, and as we’ve seen many times before, the new generation is much more savvy with the new technology.

Again, AI is still in the early days. One survey showing positive benefits doesn’t define a thesis. It will be imperative to watch this type of data over the next few years to fully contextualize the disruption caused by AI.

WSJ: Warsh Has Work To Do

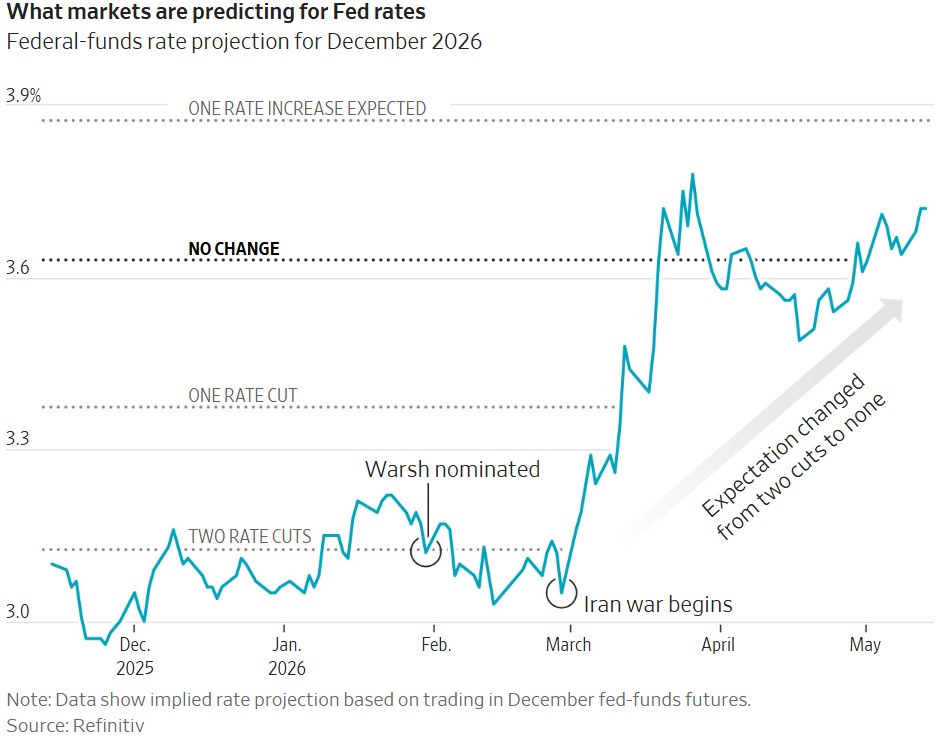

Fed rate cut expectations have been tumultuous since new Fed chair Kevin Warsh was nominated for the post at the end of January. This chart from the Wall Street Journal provides an excellent storyline summary as we approach Warsh’s first FOMC meeting as Chair on June 16-17.Fed funds futures, a market instrument that allows traders to place bets on the Fed’s policy decisions, has encapsulated this volatility. The chart below shows rate expectations based on December 2026 fed funds futures trading.

Source: The Wall Street Journal

Since the beginning of 2026, geopolitical volatility has been the main story in markets. Oil, another topic we’ve been discussing at length, is one of the main reasons why expectations have changed.

The FOMC is expressing uncertainty about its path too, with Warsh taking the reins at a key moment. Recall that at the last meeting in April, there were four dissenting votes, the most since 1992. Importantly, three votes dissented to language in the Fed’s official statement that suggested a bias toward lowering rates.

All eyes are on the upcoming June meeting, where the Fed will publish its latest quarterly update to the Summary of Economic Projections, which includes the dot plot.

It’s hard to forecast exactly how this meeting will play out—consider it an early stress test of the new Warsh Fed.

Strategas: Economic Truths

Don Rissmiller, Chief Economist at Strategas Research Partners, published several important observations this week on the state of the economy:1) We have never seen a US recession with corporate profit growth staying positive y/y. Profit growth protects capitalist economies.

2) We have never seen a US recession without the unemployment rate rising. A flexible labor market will flex (a lot) in times of trouble.

3) Recessionary weakness in the US labor market has never occurred in a vacuum. It has always been confirmed by weakness in business fixed investment. Recessions are contagion events that spread.

Q1 earnings are poised to finish the season above 25%. The unemployment rate remains well below 5%. Business investment, driven by significant AI infrastructure investments, remains positive.

These metrics matter, and Rissmiller believes they set up for a potential mid-cycle slowdown but not an end to this expansion.

Inflation remains a concern, and the Iran conflict continues to cast a cloud over inflation expectations. At the same time, the Atlanta Fed’s GDPNow forecast was revised upwards Thursday to 4.3% for the second quarter of 2026. This shows favorably against the 0.5% in Q4 2025 and 2% in Q1 2026.

We’ll continue to watch all these metrics closely, but the data continues to provide comfort about where the economy currently stands.