By: Michael Sellers

Partner, Portfolio Manager

The market’s +10% return in April from March lows was aided by improved market sentiment around the Iran conflict, but there was a more fundamental driver: Q1 earnings are coming in much stronger than expectations.

Reported S&P 500 earnings are delivering one of the strongest performances in recent years, underscoring the strength and resiliency of the US economy.

Q1 Earnings Growing at Highest Level Since 2021

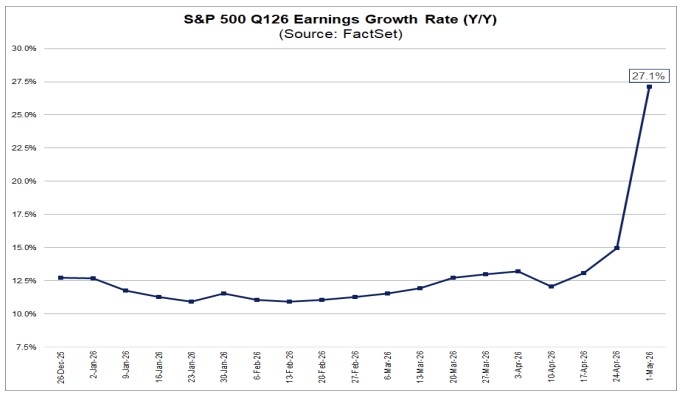

According to FactSet, the blended earnings growth rate thus far in Q1 is roughly 27%, which is more than double the 12.6% growth that was expected at the beginning of the quarter. Furthermore, if this earnings growth rate holds to the end of reporting season, this will be the strongest quarter of earnings growth since Q4 of 2021.

Source: FactSet

Leading the charge are the Communications and Technology sectors, with each sector reporting quarterly year-over-year growth of over 50%. The blended growth rate of the “Magnificent 7” increased to 61% last week, including four of the top five growth rates within the S&P 500.

A consistent theme throughout this earnings season is the continued capex commitment to AI infrastructure, semiconductors, and data-center expansion. The Communications and Technology sectors are direct beneficiaries of that theme.

Broadly speaking, earnings season is showing strong breadth, with nine of the 11 S&P 500 sectors showing positive YOY growth. Health Care and Energy are the only negative sectors thus far.

Notably, companies are becoming more efficient. Net profit margins for the quarter currently stand at 14.7%, which will be the highest net profit margin since 2009, according to FactSet.

Analysts are also increasing the projections on future earnings. Full-year calendar growth for 2026 is expected to be roughly 20%.

What Does This Mean For Investors?

First, the difference between reported earnings and expected earnings underscores the resiliency of the US economy. The first-quarter earnings strength has persisted, even amid a chaotic geopolitical environment and continued macroeconomic uncertainty.Factors including the ongoing Iranian conflict, elevated oil prices, related inflation concerns, and weaker consumer sentiment could all have weighed on profits. Yet companies have continued to deliver resilient guidance and stable outlooks.

Second, the future earnings outlook continues to improve. AI spending continues to pick up. Goldman Sachs expects the hyperscalers to spend more than $750 billion in AI-related capex in 2026 alone. More broadly speaking, full-year earnings growth guidance for 2026 now stands at 20%, which would again be the best full-year earnings growth since 2021.

Finally, the underlying strength of the US economy is still intact. The labor markets remain stable, consumer spending has proven resilient, and corporate America continues adapting effectively to an ever-changing geopolitical backdrop.

For investors, this combination of strong earnings growth, improving profit margins, and resilient economic fundamentals remains a constructive backdrop for equities moving into the second half of 2026.

Join Us On Substack

Substack is our new hub for Investment Insights, where you can easily read previous editions all in one place.If you are familiar with Substack and prefer to receive in-app mobile notifications and emails when the latest edition is published, please “Subscribe” here.

If you enjoy reading Insights on a computer or tablet, we recommend bookmarking our Substack website for an easier, more convenient experience. No email searching required, and all editions are available on the website.