Returning to a three handle is certainly a move in the wrong direction for inflation, but considering the market was expecting 3.1%, this figure was a nice, albeit small, surprise.

When we look under the hood, increased gas prices were a big driver, climbing 2.2% in the month of September. Shelter, a closely followed metric with a heavy weighting in the index, decreased on the month. Since shelter tends to exhibit slow and gradual movements, this was a notable decline in the report.

Next Fed Meeting: Oct. 28-29

The Fed’s second-to-last meeting of the year is next week, and this data is likely to support the case for continued interest rate cuts. The CPI data was a priority release since it has an impact on the cost-of-living adjustment for next year’s Social Security budget. We are still waiting for an updated report on the labor market, but we don’t expect to see that until the government shutdown ends.Given the lack of data releases, even more emphasis will be placed on the Fed’s messaging next week. The market is pricing in a nearly 100% chance of a rate cut. As we look further out, the market is pricing in additional cuts through 2026. The economic data will need to bolster this argument, however, in order for the Fed to deliver. We’ll be monitoring Fedspeak next week for clues on the future path of rates and the wind down of quantitative tightening.

Rate Cuts → Yield Curve → You

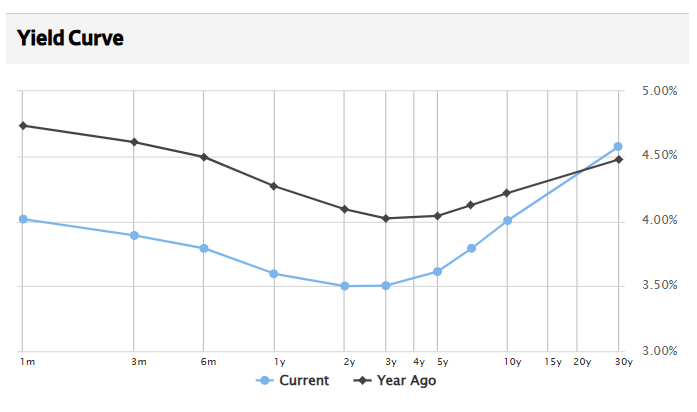

With the conversation around the Fed remaining a focal point, we’ve been paying close attention to the yield curve and the 10-year Treasury yield. The chart below shows[AW1] the Treasury yield curve one year ago (black line) against the current yield curve (blue line).One year ago, the Fed had just begun cutting rates. The curve was still entirely inverted, meaning short-term rates were higher than longer-term rates.

Today, we can see that not only has the short end of the yield curve moved lower, but the long end (in most cases) also features lower rates than one year ago.

The short end of the yield curve is dominated by the Fed’s interest rate policy, so as interest rate cuts resume, we should expect the short end to continue moving lower, steepening the curve.

Source: The Wall Street Journal

We’re paying particularly close attention to the 10-year yield. It is widely viewed as the most relevant to consumers given its correlation to mortgage rates and intermediate financing. This week, it fell under 4% for a brief period and is continuing to hover around that threshold.

Check out Head of Fixed Income Chris Gunster’s commentary from this morning about Treasury yields and changes in fed funds market expectations for deeper analysis. (Click here to read.)

We’re confident that the Fed will continue to cut, bringing the short rates lower. But for these cuts to have a meaningful impact on consumers and day-to-day business operations, we’ll also need to see the 10-year pulled lower as well. This is a key chart we’ll be focusing on as the market digests next week’s Fed meeting.