By: Michael Sellers

Partner, Portfolio Manager

Happy 4th of July everyone! Our offices will be closed on Friday, so we’re back a day early this week after being on hiatus while a key Insights contributor took a well-deserved vacation.

Despite ongoing concerns surrounding the on-again, off-again conflict with Iran, a transition in Federal Reserve leadership, and persistent uncertainty around inflation, US equity markets delivered one of their strongest quarters in recent memory.

Stocks Rebound In Q2

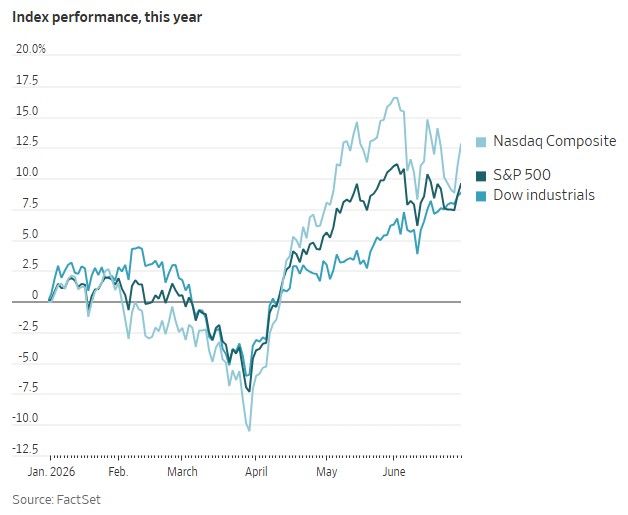

The S&P 500 rose approximately 15% during the quarter, while the Nasdaq gained roughly 21%, marking the strongest quarterly performance for both indices since 2020. According to Strategas, the S&P 500's return was the best second-quarter during a midterm election year since 1936.

Source: The Wall Street Journal

The gains were not limited to large-cap technology stocks. Small-cap stocks also participated in the rally, with the Russell 2000 Index gaining more than 21% during the first half of 2026, its strongest first-half performance since 1991.

The Dow Jones Transportation Average—which includes companies in airlines, railroads, trucking, and delivery companies and is considered a key barometer of the general health of the US economy—was up over 20% as well, signaling a broadening of market breadth.

What Is Causing The Strong Performance In Equity Markets?

The broad strength of the equity market can be attributed to several factors. First, corporate earnings have been remarkably strong and are expected to remain strong throughout the rest of 2026. First-quarter earnings grew more than 28%, while second-quarter earnings are projected to increase approximately 23%. Current forecasts call for full-year earnings growth of roughly 24%.Second, energy prices are declining as Iran and the US continue to negotiate a resolution to its ongoing conflict. West Texas Intermediate crude finished the quarter at $69.50 a barrel, down 31% from the end of Q1 and marking its largest quarterly decline since the first quarter of 2020.

Lower energy prices, coupled with expectations for further moderation ahead, helped support consumer sentiment. Consumer confidence improved to 91.2 in June from 90.6 in May. While the reading remained below market expectations of 94.2, it reflected improving household sentiment.

The labor market also remained resilient. The June jobs report showed the unemployment rate holding at 4.3%, a level consistent with a relatively healthy job market.

What Does This Mean For The Rest Of The Year?

First, the US-Iran conflict remains fluid, and investors will continue to closely monitor how developments in negotiations impact energy prices and, by extension, inflation expectations.Second, markets are becoming increasingly focused on the timeline for generating returns from the massive capex being committed to the ongoing AI buildout. As a result, earnings reports from technology companies—particularly hyperscalers and semiconductor firms—will remain under intense scrutiny.

Finally, investors are still adjusting to the early stages of Kevin Warsh's tenure as Federal Reserve Chair. The hawkish tone of his first post-FOMC press conference gave Wall Street some pause, and his stated preference for less transparency around the Fed's internal deliberations may lead to greater market sensitivity to—and interpretation of—incoming economic data.

Final Thoughts

While risks remain, the second quarter reinforced a theme that has defined much of this market cycle: investors are willing to look through uncertainty when earnings growth remains robust.The combination of strong corporate profits, improving sentiment, easing energy prices, and continued optimism surrounding artificial intelligence drove equities sharply higher during the quarter.

As we enter the second half of 2026, markets appear positioned between two competing forces—an exceptionally strong earnings backdrop and lingering macroeconomic uncertainty.

For now, earnings remain in the driver's seat, but investors should be prepared for periods of heightened volatility as geopolitical developments, inflationary trends, and Federal Reserve policy continue to evolve.