By: Chris Gunster, CFA

Partner, Head of Fixed Income

In his Forbes.com article this week, Partner and Head of Fixed Income Chris Gunster detailed how the Fed’s latest rate cut will impact interest rates and, by extension, mortgage rates and money market funds. We’re sharing an excerpt from the article below. Click here to jump straight to Chris’ full analysis on Forbes.com.

The expected interest rate decline is both good and bad. The typical American household, with both short-term investments and a mortgage, will be impacted by this in two major ways: the interest rate on the amount of money they earn from investing and the amount of money they owe on loans such as mortgages.

What’s Bad?

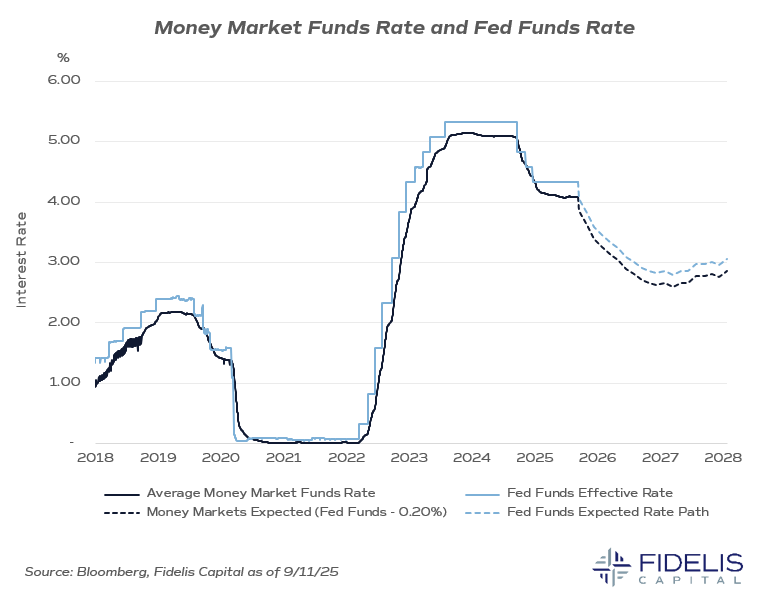

Let’s start with what is bad in a lower rate environment, money market funds. The average yield on the largest money market funds is 4.08% as of Sept. 11, according to Bloomberg and Fidelis Capital.This yield is appealing when compared to inflation. According to the most recent Consumer Price Index (CPI) release, Core CPI (all goods excluding food and energy) was 3.1% year-over-year in August. This means the average real rate (nominal yield minus the inflation rate) is about 1%.

The current high rate on money market funds has been a boon for income-sensitive investors. The Investment Company Institute reports that the amount of assets invested in money market funds is currently over $7.3 trillion, a record, and it’s up over $455 billion this year alone.

As the Fed starts to reduce interest rates, the yields on money market funds should also start to decline, more or less in lockstep. Historically, the average yield difference between the fed funds rate and larger money market funds has been about 0.20% since 2018. That is, money market funds tend to yield 0.20% less than the fed funds rate over time.

If we combine the expected future path of the fed funds rate and the average spread to money market rates, then one would expect money market fund yields to decline in the near term and move below 3% in the second half of 2026.

What's Good?

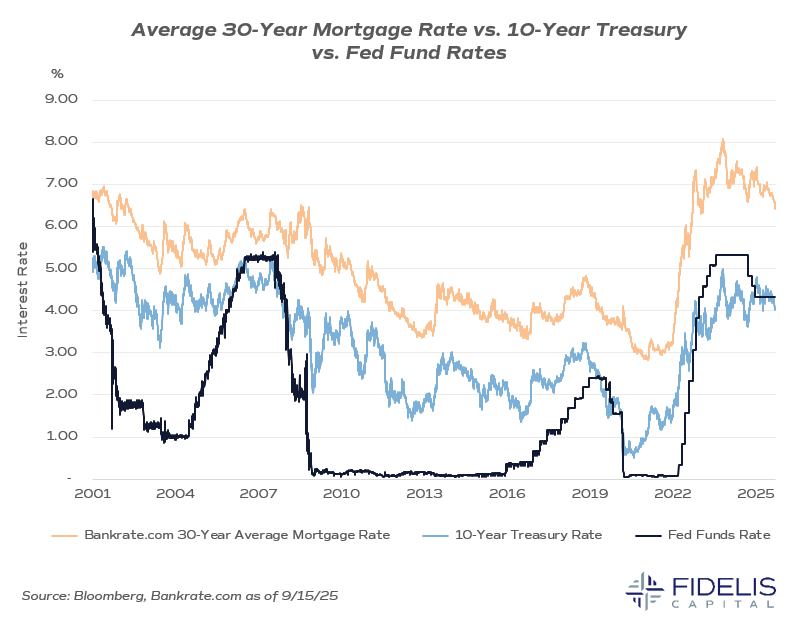

On the positive side, lower interest rates offer the opportunity to borrow money cheaper.We expect that mortgage rates will decline further in 2026, building on the initial decline this year. According to Bankrate.com, the average 30-year mortgage rate dipped below 6.5% as of September 16, 2025, for the first time since February of 2023.

Mortgage refinancing activity has started to increase, according to the Mortgage Bankers Association. As I’ve previously discussed, mortgage rates are more correlated to the 10-year Treasury yield than the fed funds rate. In the past 20 years when the Fed has cut rates, mortgage rates have declined as well, particularly at the onset of Fed rate cuts.

If the trajectory of interest rates declines as expected, then we would anticipate a pickup in real estate activity because one of the key inputs in housing affordability is lower financing costs. (See my most recent piece about the housing market for further information.)

The opportunity to refinance an existing mortgage may present itself to an increasing number of homeowners in 2026 as the likely decline in Treasury yields could push mortgage rates through 6% and potentially lower.